Brian Decker · The Wealth Society

The easy money in AI has been made.

Here's how to position for what comes next.

A 4-layer portfolio framework for the $7.6 trillion AI Supercycle.

Educational content only. Not financial advice. © 2026 Brian Decker

If you're reading this, you already feel it. Something shifted in the market this year. The portfolio that worked for the last 15 years isn't built for the next 10.

Here's where this framework came from. I spent two years tracking the actual spending, the contracts and buildouts and capital getting committed quarter after quarter. Most investors watch the AI stocks. I went looking for where the money lands once those companies spend it.

What I found: the trade has shifted. The companies most investors already own captured the easy phase. The next phase is flowing to a completely different set of companies, and most portfolios are barely positioned for it.

By the end of this guide, you'll have three things:

- The four layers every portfolio needs to capture the AI Supercycle.

- A framework for the right allocation based on the kind of investor you are.

- A simple way to see what you already own, what's missing, and where to focus next.

Read it once. It'll save you a year.

Educational content only. Not financial advice.

You haven't missed it.

You're standing at the start of it.

Right now, as you're reading this, the largest spending wave in modern history is happening.

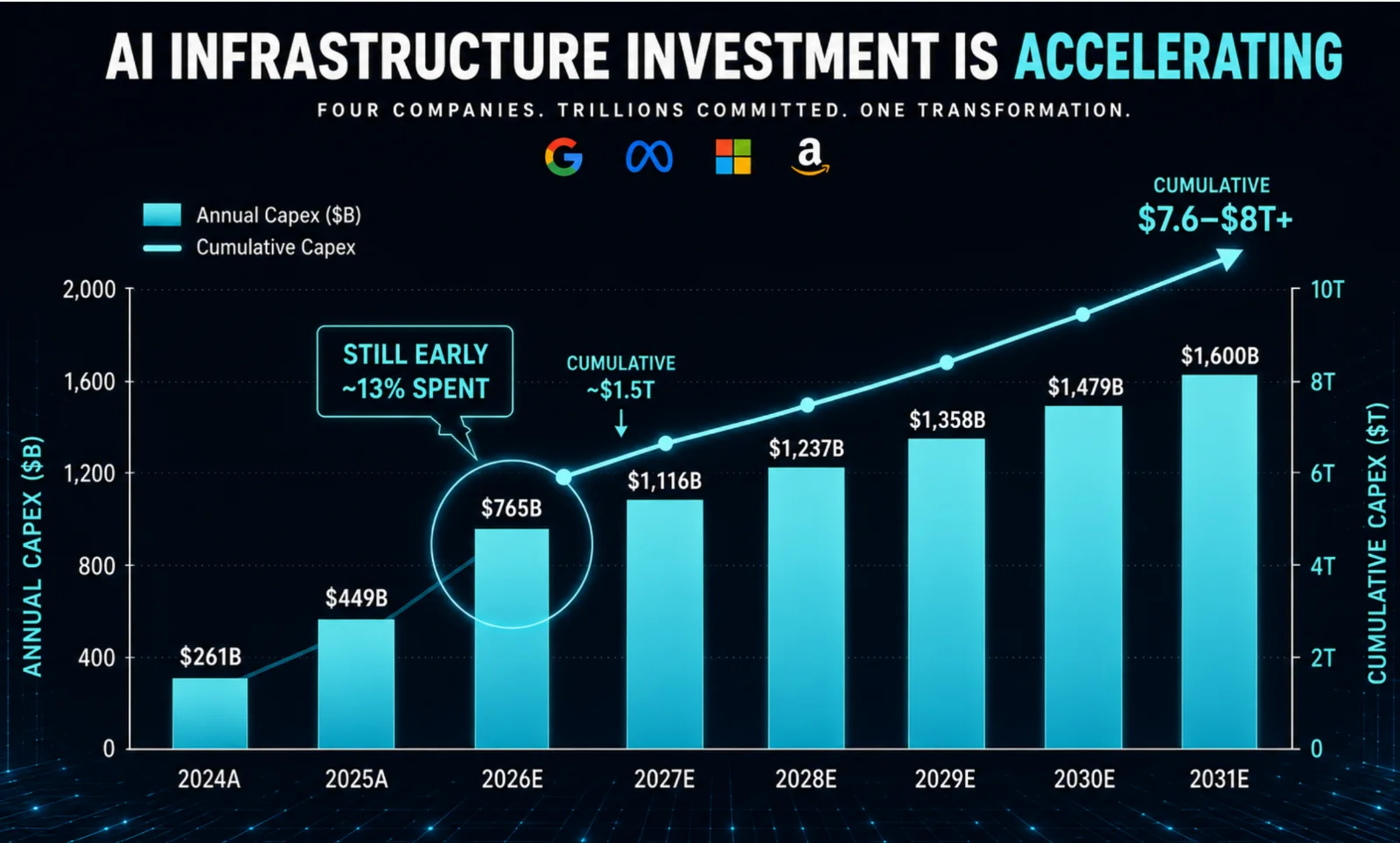

Data centers. Power. Chips. Cooling. Robotics. The metals and minerals it all depends on. None of it is "maybe." All of it is being funded, signed, and locked in this quarter. And we're barely 13% in.

That's not a forecast. That's a paid invoice.

The buildout has only just started.

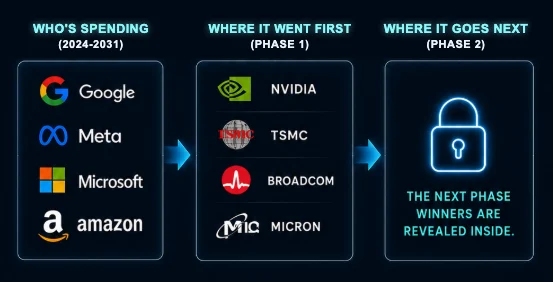

Four companies are paying for most of it. Microsoft. Alphabet. Meta. Amazon. Four of the biggest companies in the world.

2024: $261 billion. 2025: $449 billion. 2026: $765 billion. And accelerating, on pace for nearly $1.5 trillion per year by 2031. That's $7.6 trillion committed before this decade is out.

Combined annual capex · Microsoft, Alphabet, Meta, Amazon

Most portfolios are still positioned for the phase that already happened. The opportunity is to be positioned for the one that's funded and still ahead.

Educational content only. Not financial advice.

You're invested in the

companies paying for AI.

Not the ones getting paid.

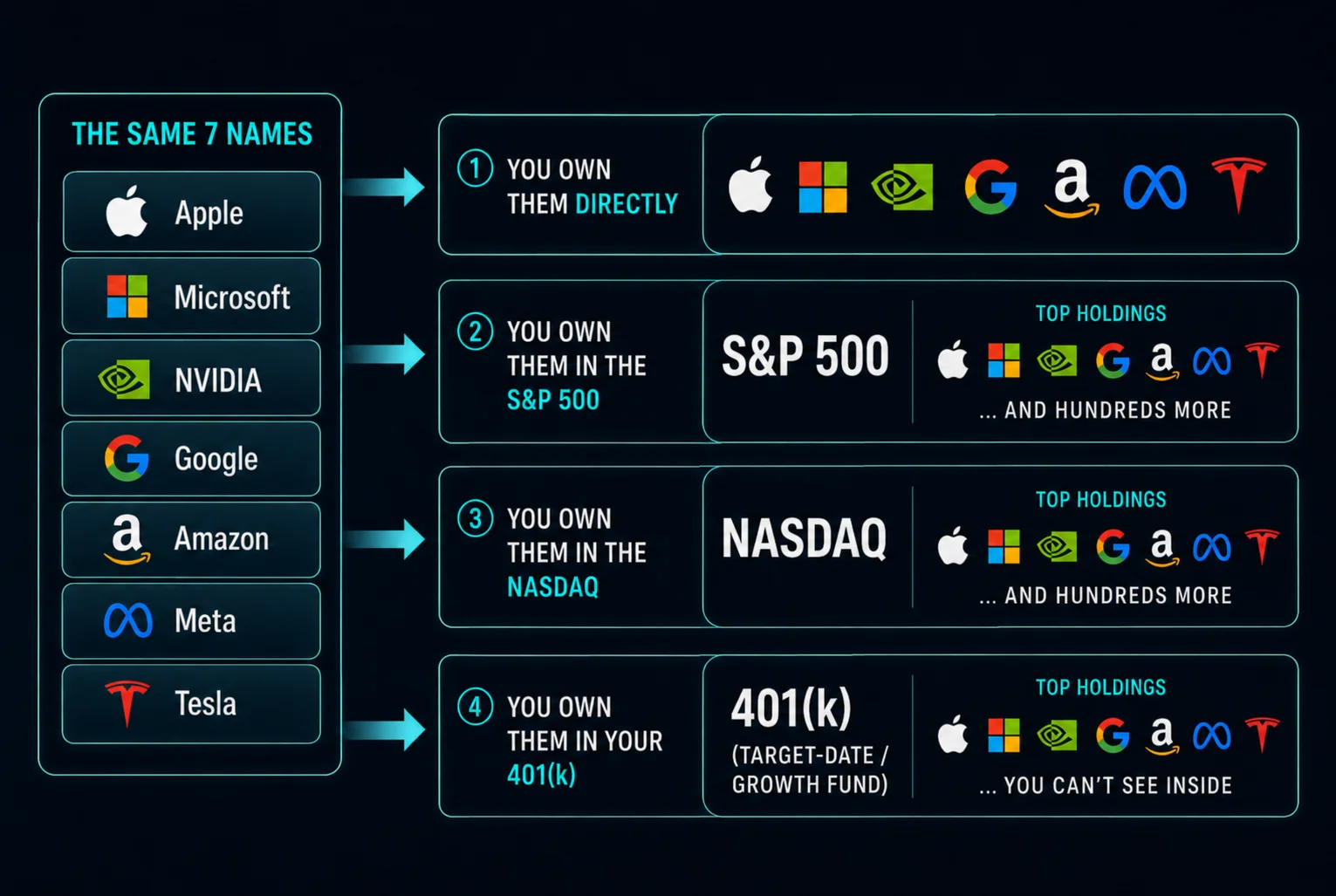

If you're like nearly everyone, your portfolio looks something like this: S&P 500 · NASDAQ · Nvidia · Apple · Tesla · Microsoft · Google · Amazon · Meta. That's the core of it. Maybe some cash on the sidelines, maybe a few other names. But that list is the engine.

It feels diversified. It isn't.

You own a few directly. Then again in the S&P 500, where those seven take 1 of every 3 dollars you invest. Again in the NASDAQ, where they take closer to half of every dollar. Again inside your 401(k), where you can't even see what you hold. Same seven names, every layer.

You're not diversified. You own one trade, four times.

The same trade everyone else owns.

Educational content only. Not financial advice.

Those seven have a name.

The Magnificent 7.

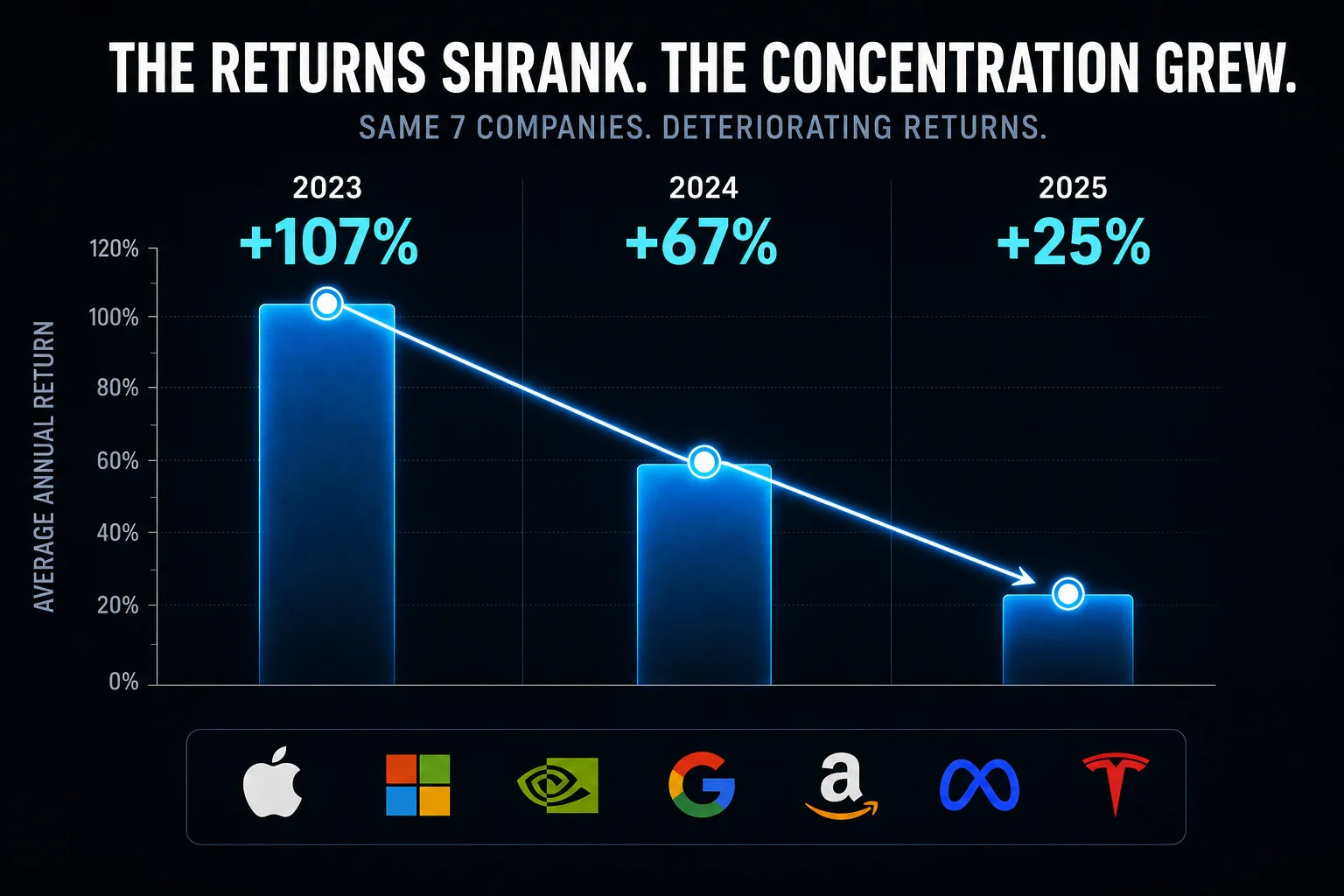

Owning them was the easiest way to beat the market for the last three years. If you held them, you made money.

Magnificent 7 · average annual return, 2023 to 2025

Most portfolios are now heavily overweight the companies that already delivered, and barely positioned for what's next.

These companies are too big to grow the way they used to. They're not the AI trade anymore. They're the ones paying for it. Even Nvidia is just the brand. It designs the chips but doesn't build most of what it sells. The suppliers do: the chip packagers, the power providers, the network builders, the supply chain that turns Nvidia's designs into revenue. That's where the next phase is flowing, and most portfolios barely touch it.

You can already see it. In May 2026, Nvidia reported the best earnings in its history. The stock sold off. Its suppliers rallied instead.

This isn't about selling everything you own. It's about trimming what's overweight and adding what's missing.

Educational content only. Not financial advice.

Before you fix it, you have to see it.

You just saw the problem in general. Now find it in your own portfolio.

You can't trim what's overweight or add what's missing until you know exactly what you're holding. Not what you think you own. What you actually own, across every account, counted as one portfolio.

An honest audit shows you two things.

- Your real concentration. The Mag 7 you bought on purpose, plus the Mag 7 hidden inside your S&P 500 fund, your NASDAQ fund, and your 401(k). Added up, the number is almost always bigger than investors expect. It looks like diversification. It's the same bet, stacked.

- What's missing entirely. The supply-chain sectors driving the next phase, the ones the indexes barely touch, usually sit near zero. You can't capture what you don't hold.

This is the moment the problem stops being about "most investors" and starts being about your portfolio.

And once you can see your real concentration and your real gaps, the next question answers itself: what should it look like instead?

That's where the framework begins.

Educational content only. Not financial advice.

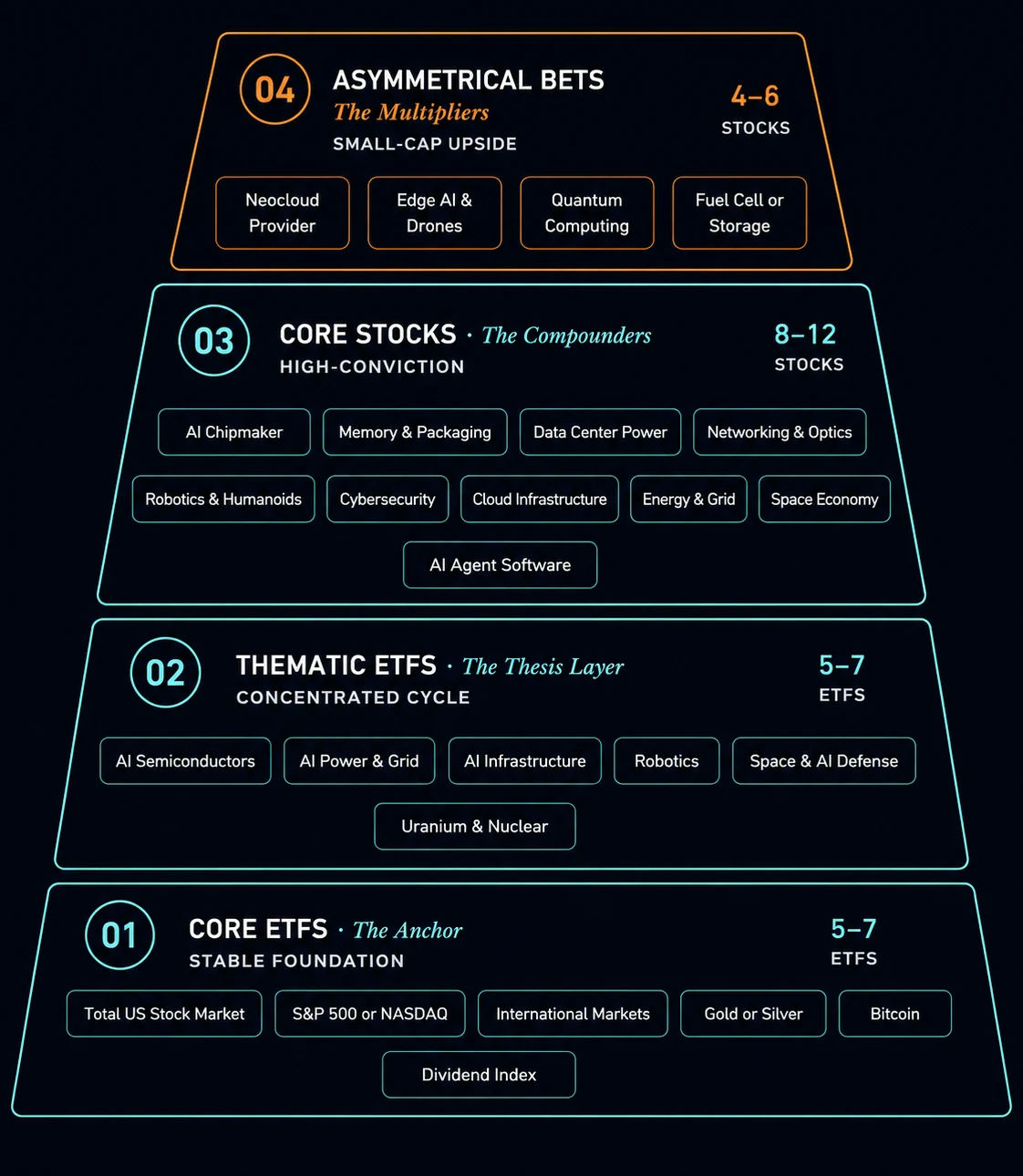

Here's what a portfolio built for this looks like.

Four layers. Each with a specific job. Built to work as one system. The first two hold ETFs, the last two hold individual stocks. Together they cover the whole cycle without stacking the same trade four times.

The stable foundation, and the largest layer. Broad-market exposure through liquid ETFs. It's there to hold the portfolio steady through volatility, so the higher-conviction layers aren't forced to sell at the wrong moment. It also already carries meaningful Mag 7 exposure, since those names dominate the major indexes, which matters when you weigh the layers that follow.

Concentrated exposure to the AI Supercycle, sector by sector, without having to pick the single winner. Each ETF holds a basket of companies inside one theme. This is the layer most portfolios are missing, and usually not because the investor made the wrong call. Most of these ETFs didn't exist when their portfolio was built.

Direct positions in the strongest companies in the supply chain. Thematic ETFs get you the sector. Core Stocks get you the leaders inside it, held at real conviction instead of the average weight an index assigns them. This is not where you stack the crowded trade. It's the supply chain the indexes barely give you, and the layer where research and patience matter most.

The smallest layer, and the highest risk. Small and mid-cap companies in emerging sectors, earlier in their growth. The math here accepts that not every position works. Some will fail. The layer is sized so a few outsized winners can still carry it. This is where the portfolio reaches for outsized upside, in categories that barely existed five years ago.

The four layers don't change. How much you put in each one does.

That weighting is what makes the framework yours, and it's where we go next.

Educational content only. Not financial advice.

The framework is the same. Your allocation is what makes it yours.

Two investors can hold the exact same four layers and end up with completely different portfolios. Neither is wrong. They're solving for different things.

Four variables set your allocation:

- Timeline to retirement. The closer you are, the more weight sits in Core ETFs.

- How you handle volatility. The mix shifts to match what you can actually hold through.

- Primary goal. Growing, protecting, or generating income each pulls the weighting a different way.

- Retirement pace. Ahead, on pace, or behind changes how hard the upside layers work.

These four interact, which is why you can't eyeball it from a guide.

The math gets personal. That's what the Wealth Profile Quiz is for. Three minutes, and it returns two things: your profile, one of six we've mapped inside The Wealth Society, and your exact allocation across the four layers. The framework you just learned, weighted for your situation.

You don't run it here. The next page is the one place that does all three, free.

Educational content only. Not financial advice.

You have the knowledge. Here's where you put it to work.

Three steps stand between most portfolios and one built for what's next. You now know all three. You could run them by hand, or run all three in one place, free.

That place is Midas. My team and I built it inside The Wealth Society to run this exact framework on a real portfolio. It is not a third-party tool. It is the same analysis we use, now free for you to run on yours.

Add your holdings and Midas runs all three:

- Audit. Your real exposure: how concentrated you are, where the same trade repeats, and which layers you barely hold.

- Framework. What you own, mapped against the four layers, so your gaps are obvious instead of theoretical.

- Profile. The Wealth Profile Quiz returns your investor profile and your exact allocation across the layers.

The whole thing takes about 15 minutes, most of it just entering what you own.

What you find is usually a few adjustments, not a teardown. Trim what's overweight. Add what's missing.

The guide gave you the knowledge. Midas is where it becomes your portfolio.

Educational only. Not personalized financial, investment, tax, or legal advice. Frameworks and themes are illustrative for research, not buy or sell recommendations. All investments carry risk, including loss of principal. Company names and logos are trademarks of their respective owners, shown for identification and educational purposes only. No endorsement or affiliation is implied. © 2026 Brian Decker.